Thinking about a neighborhood where parks, trails, and community spaces are part of everyday life? That is the promise of many master‑planned communities. If you are curious about how that model works and what to look for at The Promontory, you are in the right place. You will learn the basics of master‑planned living, what to verify about amenities and fees, and how to prepare as a buyer or seller. Let’s dive in.

What is a master‑planned community

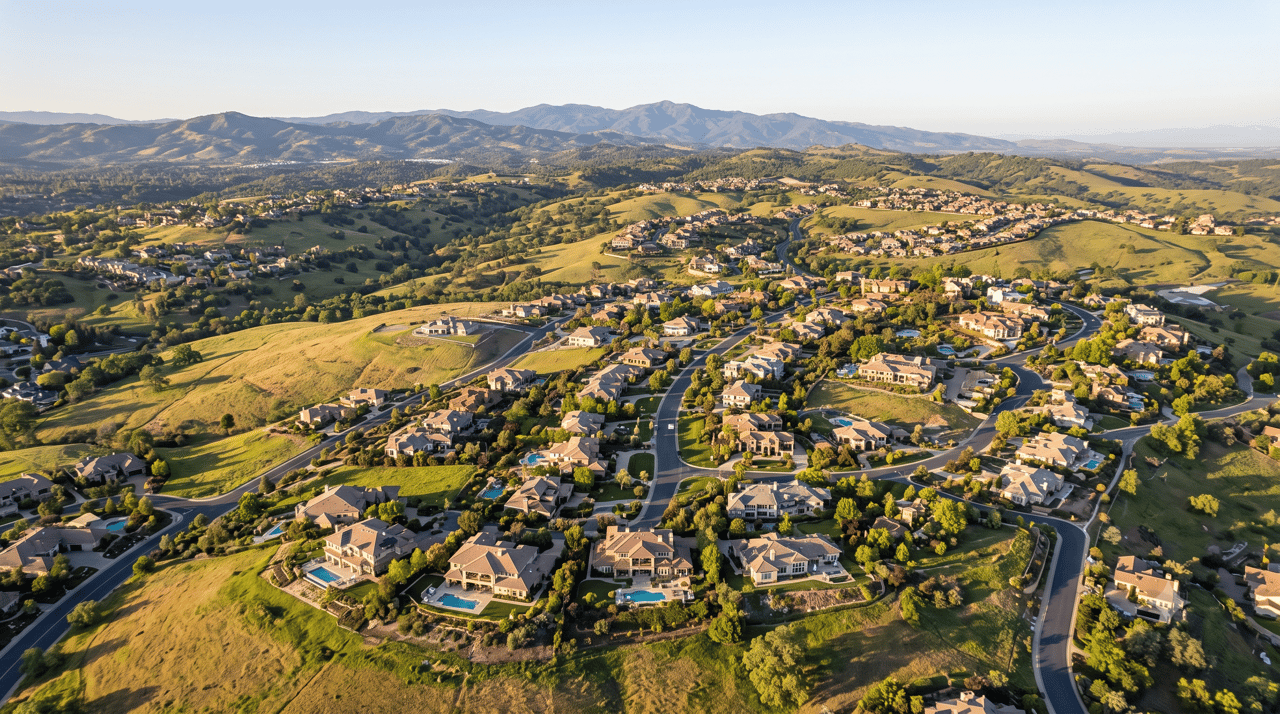

A master‑planned community, often called an MPC, is a large residential area designed and built under one long‑range plan. It typically mixes housing types with parks, trails, and sometimes retail or club facilities. Most MPCs are built in phases over several years and operate with a homeowners association. Many also have sub‑associations for specific neighborhoods.

Why buyers choose MPC living

You get a cohesive neighborhood look and feel, with design standards that help maintain curb appeal. Common areas are cared for by an association, which keeps parks, entries, and streetscapes tidy. Amenities can support an active lifestyle and a strong sense of community. If that fits your goals, The Promontory may be worth a closer look.

Amenities and lifestyle to expect

Common amenities in MPCs include parks, walking and biking trails, fitness centers, pools, tennis or pickleball courts, and community gathering spaces. Some also offer golf, equestrian facilities, dining, or on‑site retail. Community programming can include classes, events, and clubs that make it easier to meet neighbors.

Membership and access models

Not every amenity is included in HOA dues. Many communities operate separate, fee‑based club memberships, which can involve initiation fees and monthly or annual dues. In some cases, membership is optional, and in others it may be required. Always confirm what your HOA dues cover, whether club memberships are separate, and if memberships can transfer with a home sale.

Guest and rental rules

Amenity use often follows specific rules, such as guest limits, reservation windows, and quiet hours. If you plan to rent your home, check how guests or tenants can access amenities and whether short‑term rentals are allowed. These rules live in the HOA’s CC&Rs and any club membership documents.

Housing types and design standards

MPCs tend to offer a mix of single‑family homes, townhomes or condos, and sometimes custom lots or estate properties. You will also find design review guidelines that control exterior changes, landscaping, and additions. These standards protect the community look and can support resale value over time.

New construction vs. resale

Depending on the buildout stage, you may see a blend of builder homes, custom properties, and resales. If the developer is still active, there may be ongoing construction and phased amenity rollouts. If the community is complete, governance often shifts more to homeowners through the association board.

HOA, CC&Rs, and fees

Buying in an MPC means agreeing to CC&Rs, which spell out property use and responsibilities. Rules often cover exterior modifications, parking, pets, landscaping, and rental policies. Fees can include master HOA dues, possible sub‑association dues, and sometimes separate club dues and initiation charges. Some areas also use special districts that add line items to your property tax bill to fund infrastructure.

What to request before you buy

- CC&Rs, bylaws, and rules and regulations

- Annual budget, audited financials, and the latest reserve study

- Resale certificate or estoppel letter showing current dues, assessments, and violations

- Design guidelines and architectural review process

- Club membership agreement and current fee schedule, if applicable

- Recent HOA board meeting minutes and any litigation disclosures

- Insurance summary for the master policy

Financing and insurance in an MPC

Lenders review association financials, rules, and any litigation. If you are buying a condo or townhome, there may be agency eligibility rules. Title and closing costs can include transfer or initiation fees in some MPCs, so ask early. On insurance, understand what the association’s master policy covers versus what your homeowner policy must cover, and review any special exposures such as wildfire, flood, golf course, or open‑space adjacency.

Lender and title considerations

- Ask your lender how mandatory dues and any club fees factor into approval.

- Confirm whether any transfer or initiation fees apply at closing.

- Verify how rentals are treated, since rental limits can affect underwriting.

Resale and marketability factors

Well‑maintained amenities, strong reserves, and consistent design standards can help support resale value. High fees, frequent special assessments, or unclear governance can be drawbacks. Your agent should compare inside‑the‑community comps with nearby alternatives to show how The Promontory performs in the local market.

The Promontory: what to verify

Use this quick checklist to focus your questions and document requests specific to The Promontory:

- Amenities and access: full list of amenities, what HOA dues include, and whether club membership is separate or required

- Membership terms: initiation and recurring fees, guest rules, rental and transfer policies

- Governance: CC&Rs, bylaws, design guidelines, and status of developer control or turnover to homeowners

- Financial health: current dues, audited financials, reserve study, and any pending or recent special assessments

- Fees and taxes: master and sub‑association dues, any transfer fees, and any special district or assessment taxes

- Insurance: master policy coverage versus owner responsibilities

- Property and hazards: flood zone status, wildfire risk, and who maintains roads, trails, and stormwater systems

- Schools and services: assigned schools and proximity to everyday services, verified through official sources

- Commute and access: typical drive times to major job centers and nearest transit or airport

- Market snapshot: recent sales, days on market, active inventory, and price trends drawn from the local MLS

Buyer checklist for The Promontory

- Get the HOA resale certificate, financials, reserve study, and design guidelines.

- Confirm amenity access rules and any separate club membership costs.

- Ask about upcoming capital projects or planned assessments.

- Review rental rules and minimum lease terms if renting is part of your plan.

- Check insurance requirements and any special exposures relevant to the area.

- Compare Promontory comps with nearby communities to understand value.

Seller checklist for The Promontory

- Gather CC&Rs, rules, design guidelines, and the HOA resale certificate.

- Confirm any transfer fees or membership rules that could affect closing.

- Prepare amenity highlights and community calendar details to market lifestyle benefits, following HOA photo and access guidelines.

- Coordinate with your agent on timing, pricing, and professional presentation.

- Disclose any known assessments, violations, or pending projects.

How to build a local market snapshot

For an accurate read on The Promontory, pull recent closed sales, active listings, average days on market, and months of inventory from the local MLS. Pair that with the current HOA and any club fee schedules from the association or club documents. Numbers change often, so update the data right before you make an offer or go live with a listing.

Potential pros and cons to weigh

Pros

- Amenity access, community programming, and a cohesive neighborhood feel

- Managed common areas and design standards that can help support long‑term value

- Built‑in social and recreational opportunities

Cons

- Higher recurring costs when HOA dues and separate club fees both apply

- Possible special assessments if reserves are low or amenities age

- Rules on exterior changes and rentals that may not fit every owner

- Ongoing construction in earlier phases that may affect daily life

Next steps

The best move is to verify current documents and fee schedules before you decide. If you want a clear, concierge‑level plan for buying or selling in The Promontory, reach out. With direct access to your broker and a hospitality‑first process, you will get confident answers and a smooth path from offer to closing.

Ready to talk through your goals at The Promontory? Connect with Tiegen Boberg for personal, white‑glove service.

FAQs

What is a master‑planned community and how is it different from a typical subdivision?

- An MPC is a large community built under one long‑range plan with shared amenities, design standards, and an HOA structure, while a typical subdivision may have fewer amenities and less centralized planning.

How do HOA dues and club fees usually work in The Promontory?

- Dues and fees vary by community; confirm what HOA dues cover, whether there is a separate club with initiation and recurring fees, and how membership transfers at resale by reviewing the HOA and club documents.

Can I rent my home in The Promontory and still use amenities?

- Rental and amenity access rules are set by the CC&Rs and any club agreement; verify minimum lease terms, short‑term rental rules, and guest or tenant access policies before you buy.

What insurance should I consider for a home near open space or a golf course in an MPC?

- Review the HOA’s master policy and talk with your insurance provider about what your policy must cover, including any exposures related to open space, golf course adjacency, wildfire, or flood risk.

What documents should a seller in The Promontory gather before listing?

- Collect CC&Rs, rules, design guidelines, the HOA resale certificate, financials and reserve study, any club membership documents, and details on transfer fees or assessments to streamline buyer due diligence.